It's a Money Thing

Discover a valuable resource for you, your family or your classroom. It's a Money Thing offers a wide range of humorous but effective financial literacy videos, downloadable handouts, and informative infographics. Whether you're seeking a refresher on financial topics or looking for comprehensive resources on financial literacy, you can find it all here.

You can also request our very own Financial Education Specialist to visit your school, non-profit, after school program or business to teach a financial well-being lesson!

Request a PresenterEducational Videos

Budgeting & Saving

Budgeting Basics

Whether you're planning your first budget or re-evaluating your current budget, these ground rules will set you up for success. It doesn't matter if you manage your budget on your smartphone or if you prefer good ol' pen and paper— these budgeting basics can be applied to every budgeting system.

Building a Budget

No two budgets are alike. The same expense— whether it's a book, a phone bill, or a tank of gas— can mean different things to different people. To explore this concept, take a look at how even the simplest categories can be considered a need, a want and/or a savings goal.

Guaranteed Deposits

Investing in certificates can be a safe and reliable alternative to investing in the stock market for young adults. Certificates provide a guaranteed rate of return, are backed by the NCUA or FDIC, and offer a predictable income stream. They are ideal for those who are risk-averse or who prefer a steady income stream.

Saving with New Skills

Mastering domestic skills can save you money— the more you can make or repair yourself, the less you will have to spend on goods and services. When you do need to buy things, skills like budgeting, couponing, and deal-hunting help you get the most bang for your buck.

Navigating Income Loss

The stress of losing a job not only affects your finances— it can also take a toll on your mind and body. The path to recovery includes stops along the way to scrutinize your options, downsize your spending and energize your spirit.

Responding to Financial Emergencies

In some cases, an unpredictable event can convert regular expenses into emergency expenses. Although there isn't a one-size-fits-all solution to financial emergencies, there are steps you can take that will minimize damage while you work on a recovery plan.

Avoiding Lifestyle Creep

Lifestyle creep is the tendency to spend more money as your income increases. Lifestyle upgrades can quickly become part of your routine spending, blurring the line between "luxury" and "necessity." This means that the dollars that could be going toward your savings goals get swallowed up by day-to-day spending instead.

Paying for Pets

A pet's companionship is priceless, but its expenses add up fast. Like walking the dog or scooping out the litter box, budgeting is a part of basic pet care. Preparation in the form of monthly saving and and creating emergency funds will help enrich you and your pet.

Emergency Fund Boot Camp

An emergency fund is an essential part of your personal finances. Its importance is often mentioned, and yet 26% of Americans currently have no emergency fund in place. Of those who do have an emergency fund, up to two-thirds do not have the often-recommended six months' worth of expenses saved up.

Good vs. Bad Spending

If you're waging an inner battle of good vs. bad every time you whip out your credit card or peek at your monthly bank statement, it's probably time to give your views on budgeting a shake-up. There are good and bad ways to spend money, just as there are good and bad ways to save it.

Comparing Cards

It's a decision that comes into play for every bill you pay, every tank of gas you buy, and every coffee you pick up on the way to class or work. Cash, check, or card? Debit, credit, or prepaid debit? It pays to be smart about when to use each payment type and to understand the differences between them.

Living on Your Own

Living on your own for the first time can be empowering. It means having independence and all the things that come with it. Some of those things— like not having to share a bathroom— are wonderful. Others— like killing spiders yourself— are not so fun. And leading the pack in the not-so-fun category: bills.

Common Money Beliefs

How did you decide where to open your first bank account? Where did you learn to budget? If you have a money question now, what do you do? Most young adults don't receive any kind of formal financial education. So, it's likely that you'll need to seek guidance when it comes to money management.

How to Save on Groceries

Grocery stores are designed to make you slow down and wander around— and spend more money in the process. The average American household spends $4,643 a year on groceries. Here are some tips to help you take a bite out of your grocery bill!

Pay Yourself First

Paying yourself first is a simple but effective strategy for saving up for your long-term goals. As soon as you get paid, put money into your savings account first— the size of that contribution is up to you, but even small amounts will add up over time.

Retirement & Budgeting

The 4% rule provides a helpful framework for retirees planning their withdrawal strategy. While it offers a solid starting point, it's important to consider individual circumstances, market conditions and potential adjustments. Consulting with a financial advisor can help tailor the 4% rule to your specific needs, ensuring a more secure and sustainable retirement.

Give Every Dollar a Job

Don't leave your dollars just laying around. You've got to give every dollar a job! That way, your needs and goals are taken care of and extra spending money is stress-free.

Watch Out for Sneaky Expenses

Even when your monthly spending seems like smooth sailing, make sure to keep an eye out for sneaky expenses. Things like unused online subscriptions, expensive gifts for friends and family, recurring charitable donations and high bank fees can sneak up from behind and torpedo your budget.

Save for Emergencies

Budgeting your balance with your auto pay schedule? Don't face an unexpected car problem, vet bill, or disaster by asking "what am I going to do?" Save for your emergency fund before you need one.

Grades K-6

Making Money

Thinking about what you want to be when you grow up means also thinking about what kind of income your dream job will have. Your career should be an equal combination of three things: income, skills, and passion.

Spending Money

You make many choices every day. You choose how to spend your time. You choose how to spend your energy. You also choose how to spend your money.

Saving Money

Saving money is an important skill to develop. It can remind you of what's important, makes it easier to choose saving instead of spending, and gives you something to look forward to.

Borrowing Money

Borrowing money comes at a cost. This extra cost is called interest. If borrowing money costs more, why do people still do it?

Giving Money

Giving away a small portion of your savings can make a big difference to a cause that you care about. For most people, spending comes naturally, saving up for something special is harder, and setting money aside for giving is really hard.

Growing Money

Many financial experts suggest that your money should be growing somewhere between 5% and 10% per year. You won't get that from a savings account these days.

General Information

Credit Union Myths

Even though there are over 5,000 credit unions in the United States, misconceptions about their structure and services still exist. Some people mistakenly believe that credit unions are limited, compared to big banks. We address four persistent credit union myths.

Choosing Your Financial Institution

Banks and credit unions offer essentially the same products and services, but they operate differently. Despite this, many people put more thought into building their Netflix queue than they do choosing their financial institution. Whether you're just starting out or rethinking your current financial setup, here is what you need to know.

Co-operative Principles

Credit unions are unique depository institutions created not for profit, but to serve their members as credit co-operatives. They put their values into practice by following the 7 co-operative principles. This sets credit unions apart from all other financial institutions, strengthens the community, and benefits you too!

Working From Home

Working from home promotes work-life balance, but it does not guarantee it. Even though it cuts out your commute and gives you flexibility with your time, it can still lead to anxiety, distraction, and burnout. Setting clear boundaries between your work time and your personal time promotes a healthy work-life balance

Know Your Checking Account

Balancing your checkbook gives you power— the power of knowing exactly how much money is available to you. Whether you use a checkbook register, a spreadsheet on your computer, or an app on your mobile device, balancing your checkbook is a good habit to form.

Earning Money Online

It's hard to ignore the appeal of making real money online. While some of us dream of a wildly successful Internet career, the rest of us are happy to settle for online earnings that are a little more modest. Thousands of money-making opportunities are just a web search away.

Acing the Job Interview

In preparing for a job interview, it's easy to focus on how you're meeting others' expectations of you instead of considering what expectations you have for your next job and future employer. Despite its unknowns and stresses, the job interview is ultimately an empowering experience that brings you closer to your career goals and life goals.

Grow Your Money Locally

Did you know that your personal finances can make an impact in your neighborhood? Small changes in how you save and spend your money can better your community and the environment. Local retailers and restaurants do more for the local economy than their national chain competitors.

How to Save on Tuition

School is important. It's also expensive. When they graduate, the average student loan borrower has a $37,172 debt. Offset the costs of post-secondary education the smart way by using free money, your money, and borrowed money (in that order).

Owning vs. Renting a Home

There are key differences between owning and renting a home. Owning a home gives you the peace of mind of having a permanent place to live. As a renter, it's relatively easy to move around; you're not responsible for finding a new tenant to take your place. There's no right answer for whether it's better to own or rent your home.

Writing a Business Plan

Writing a business plan is an essential part of building a successful business. At its core, a business plan is a road map for your project: it establishes your purpose, it sets goals and expectations, and it forecasts the relationship between cost and revenue.

Income & Investments

Income Essentials

How much money will you make? Your income is influenced by four interconnected factors: career, education, skills, and trends. Where you work, your education level, current skills, and the ever-changing trends in the world economy all interact and have an impact on your current and future income.

Compound Interest Mind Bending

Compound interest is easy to understand: compound interest = more money for you! Those who can potentially benefit most from it (those in their teens and 20s) don't seem to be taking advantage of it. Savings contributions and retirement savings participation rates are falling among young adults.

Investment Vehicles

Investing can seem like a very risky, complex and fast-moving process. With endless combinations of investment vehicles to choose from, it can be difficult to take your first step as an investor— especially with the knowledge that all investments carry the risk of losing some or all of your money. So why bother?

Understanding Inflation

Inflation refers to the rate of change or increase in the average prices of goods and services typically purchased by consumers. When the price level rises, every dollar you have buys a smaller percentage of a good or a service. While prices may seem to rise slowly, the effects of inflation really add up over time!

Compound Interest Rule of 72

The Rule of 72 is a handy tool to quickly estimate how many years it will take to double your investment at a given rate. The Rule of 72 works with investments that have compounding interest. You simply divide 72 by your annual interest rate. What results is an approximation of how many years it will take for you to double your investment.

Trends in the Stock Market

Trends in the Stock Market explains the differences between "bull and bear" markets and discusses how both upward and downward trends represent opportunities to make money. Trends can be short term, intermediate term, or long term, and can apply to the market as a whole or to a single stock or commodity.

Saving for Retirement

Saving for retirement poses some unique challenges: How are you supposed to prioritize retirement savings against the long list of more immediate goals? How are you supposed to find the motivation to prepare for something that's decades away? How can you quantify the amount you will need to save when you have no idea what your future will look like?

Decoding Cryptocurrency

Cryptocurrencies have emerged in recent years, causing a whirlwind of confusion. Whether you're a seasoned investor or just beginning to explore, this new digital realm can be perplexing. What are the things you should know about crytocurrencies?

After Grad: Work or College?

Choosing a path to pursue after graduation can leave you feeling directionless. Whether you start out by getting a degree or by joining the workforce, your career path should be designed to lead you to your dream job. Here are some factors to consider, whether you're thinking of hitting the books or the job market after graduating.

Let's Talk Taxes

Your pay stub is more than just proof of income. It allows you to better understand your personal finances and to make informed decisions when it comes to budgeting and tax time. Although all pay stubs contain the same basic information, the layout and wording can vary. There may also be additional taxes and deductions unique to your city or state.

Retirement and Savings

Retirement planning can be a complex endeavor. As you approach your retirement years, it becomes increasingly important to organize your financial affairs effectively.

Retirement and Taxes

Diversification isn't limited to your investment portfolio. If you're actively saving for retirement, consider diversifying how and when your savings will be taxed.

Retirement and Estate Planning

Having a well-prepared last will and testament can greatly simplify any legal challenges that may arise after your death. It's also wise to review your will periodically and update it as circumstances change.

Invest Early

Investing is pretty intimidating. Thinking of waiting and starting it in a few years? Then you've got to start investing early. The earlier you start saving, the more time you'll have to earn from interest.

Dollar Cost Averaging

Instead of investing a lump sum all at once, you can invest a smaller consistent amount at set intervals, like once a month, once a paycheck or every Tuesday. This will average out your cost, so you can stop worrying about day-to-day fluctuations in your investment, and look at the big picture.

Concentration Risk

What do you know about concentration risk? The more concentrated your investments are in a certain company, market segment or asset class, the higher your risk of steep losses. Instead, you want to build a diversified investment portfolio that spans different companies and industries, and includes a variety of different assets.

Loans

Loan Basics

Applying for a loan requires a lot of research— not just on loan specifics, but research on you too! Loans make some of our biggest life decisions possible, so it's crucial to be realistic about your goals, your financial situation, and your future.

Buying a Used Car

If you take your time to carry out an inspection plus research a vehicle's history, buying a used car can be rewarding and cost-effective. Research your options, inspect the car you're looking to buy, and negotiate a price.

Leasing vs. Buying a Car

When it comes to buying a new car, you have three options: purchasing it with cash, purchasing it through a loan (also known as financing), or leasing it. For most shoppers, the decision comes down to buying or leasing. The decision to lease or to buy a new car will have an impact on your finances as well as your lifestyle.

Predatory Lending

Predatory lending can also take the form of car loans, sub-prime loans, home equity loans, tax refund anticipation loans, or any type of consumer debt. Common predatory lending practices include a failure to disclose information, disclosing false information, risk-based pricing, and inflated charges and fees. These create a cycle of debt and severe financial hardship.

Demystifying Mortgages

Buying a home is likely the biggest purchase of your life, and you'll usually need a loan to make it happen. Comparing mortgages can be confusing and intimidating— let's break it all down so you can understand how it works and what happens in the mortgage repayment process.

Student Loans

If you're considering financing your college education with the help of a student loan, the smartest thing you can do for yourself is to only borrow what you truly need. You're making decisions and opening up possibilities that will shape your future— a future that is fulfilling and that decidedly does not include years of crippling debt.

Using Your Credit Card

By using credit responsibly, you're contributing to your credit history, which will make it easier and more affordable to secure a loan in the future. By paying in full and on time, you avoid carrying a balance on your card, which means the credit card company cannot charge you interest on your balance.

Strategies for Debt Repayment

Debt is stressful, it's expensive, and it limits the amount of money you can put toward your life goals. To pay off your debt, get organized by making a list of all your debts, choose a strategy which affects the order in which you pay off your debts, and follow a monthly payment plan that is generous and realistic.

Snowball vs. Avalanche

How should you approach paying off debt? The Snowball method pays off the lowest balance first, then moves on to the next lowest balance until you're out of debt. The Avalanche method starts with the balance that has the highest interest rate, then moves on to the next highest rate until you pay everything off.

Debt Consolidation

If you find yourself burdened by a bunch of different debt, consider consilidating it. By consolidating your debt, you pack a bunch of smaller debts into one big debt with a lower interest rate. This will save you money and help you get back on the path to being debt-free.

Don't Give Up on Your Debt

Does dealing with debt seem too difficult? It helps to look at your monthly budget and make a debt repayment plan. If you can, pay more than the monthly minimum to pay down your principal balance quicker, and if you receive any financial windfalls, use them to pay off debt rather than treating them as spending money.

Pay in Full, Pay on Time

Don't just make the minimum monthly payment on your credit card. Make sure you can pay your balance in full and on time. Saving up ahead of time and making all payments fully will stop your card from being saddled with debt and interest.

Leave Some Room

It's best to stay away from your credit limit. In order to build up a good credit history, you want to be using 30% or less of your total credit. Keeping your utilization rate low will also help prevent your credit card debt from piling up faster than you can pay it off.

Review Your Statement

Have you checked your credit card statement lately? It's important to check your credit card statement every month to track your spending, and to watch for any incorrect charges. Being informed about your statement will keep you financially aware.

Looking at Loans

Before taking a loan, one should always shop around. A fixed-rate loan may have a higher interest rate, but the payments will be consistent, and easier to budget for. An adjustable-rate or variable-rate loan may offer a lower interest rate to start, but your monthly payments might increase as the interest rate fluctuates.

How Much Should I Borrow?

Do your homework and figure out how much home you can afford, based not only on the monthly mortgage payments, but also on all of the other expenses, such as property taxes, insurance, homeowners association fees, and utilities, to name just a few.

Don't Rush Into a Loan

You should never borrow in the moment. Always take some time to think, and assess. Make a solid plan to pay back your loan in full, and if you have extra money, make additional payments whenever possible to save on your total interest. You also need to account for any extra expenses you might run into.

Credit Scores

Breakdown of a Credit Score

Credit Scores are used by financial institutions and credit card companies to determine risk level when issuing you a loan or a credit card. What do you actually know about them? How long have they been around? And what's the deal with checking them?

Boost Your Credit Score

Many people believe that improving a credit score is a matter of trial and error and, as a result, there's a lot of "credit score advice" floating around that can end up doing more harm than good. This video will help debunk four of the common credit score myths that you might come across.

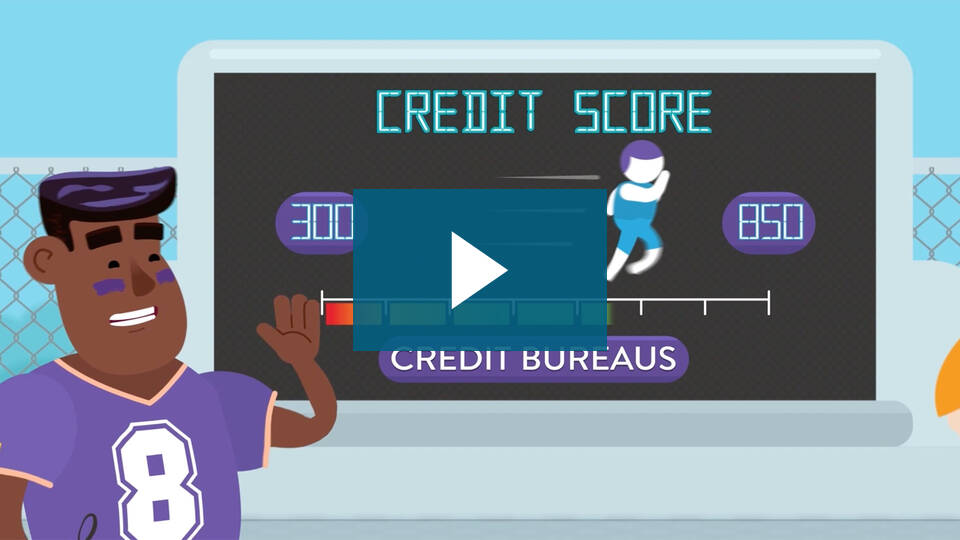

What Is a Credit Score?

What's a credit score? A credit score is a three-digit number between 300 and 850 that's calculated by credit bureaus. The higher your score, the better you look to potential lenders. Basically, a credit score rates your creditworthiness and it's all based on the info in your credit report.

Why Do I Have a Credit Score?

Not quite sure why you have a credit score? Your credit score helps predict the likelihood of you making on-time payments. Your credit report contains info on your use of credit over time, and that info goes through a scoring model that calculates your credit score. If you keep your score up, it can give you more options and save you a ton of money!

How is My Credit Score Calculated?

Does looking at your credit score seem complicated? Why is it that number? Your credit score is calculated based on your history of on-time payments, how much of your credit capacity you use, how long you've had a credit history, how many new credit accounts you open and the variety of different types of credit that you use.

Security

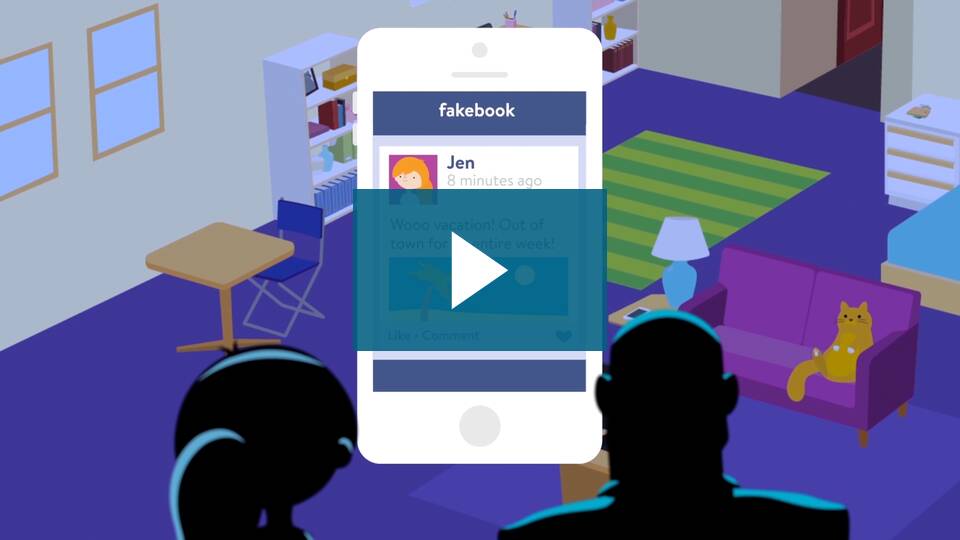

Foiling Identity Theft

Identity theft is nothing new, and yet it still manages to cost its victims billions of dollars globally each year—not to mention the time and hassle involved in recovering a stolen identity. Here are the top five information jackpots for identity thieves, along with helpful tips on what you can do right now to protect yourself.

How to Spot Scams

Whether it's online, over the phone or in person, scammers are always coming up with new ways of influencing their targets. By staying calm in high-stress situations and by giving ourselves a little extra time to think, we're better able to spot recurring scammers' favorite tactics and save ourselves from making costly mistakes.

Intro to Insurance

Insurance is a contract in which an individual or entity receives financial protection or reimbursement against losses from an insurance company. The insurance company pools clients' risks to make payments affordable for the insured.

Organize Your Finances

Every year, it's nice to do a bit of "financial spring cleaning" and declutter your filing cabinet, your desk drawers, and the various hiding places where miscellaneous scraps of paper tend to accumulate and multiply. Find out what you should be saving, and what's OK to shred.

Lesson Plans

It's A Money Thing lesson plans include learning objectives, instructions for teaching the lesson, group activities, and quizzes with answer sheets to bring financial literacy into your classroom.

- Acing the Job Interview Opens in new tab. Link is a PDF document.

- After Grad: Work or College? Opens in new tab. Link is a PDF document.

- Boost Your Credit Score Opens in new tab. Link is a PDF document.

- Breakdown of a Credit Score Opens in new tab. Link is a PDF document.

- Budgeting Opens in new tab. Link is a PDF document.

- Building a Budget Opens in new tab. Link is a PDF document.

- Buying a Used Car Opens in new tab. Link is a PDF document.

- Choosing Your Financial Institution Opens in new tab. Link is a PDF document.

- Common Money Beliefs Opens in new tab. Link is a PDF document.

- Comparing Cards Opens in new tab. Link is a PDF document.

- Compound Interest Opens in new tab. Link is a PDF document.

- Debt Repayment Strategies Opens in new tab. Link is a PDF document.

- Demystifying Mortgages Opens in new tab. Link is a PDF document.

- Earning Money Online Opens in new tab. Link is a PDF document.

- Emergency Fund Boot Camp Opens in new tab. Link is a PDF document.

- Exploring Money Beliefs Opens in new tab. Link is a PDF document.

- Foiling Identity Theft Opens in new tab. Link is a PDF document.

- Good vs. Bad Spending Opens in new tab. Link is a PDF document.

- Grades K-6

- How to Save on Groceries Opens in new tab. Link is a PDF document.

- How to Save on Tuition Opens in new tab. Link is a PDF document.

- How to Spot Scams Opens in new tab. Link is a PDF document.

- Income Essentials Opens in new tab. Link is a PDF document.

- Intro to Insurance Opens in new tab. Link is a PDF document.

- Investment Vehicles Opens in new tab. Link is a PDF document.

- Know Your Checking Account Opens in new tab. Link is a PDF document.

- Leasing vs. Buying a Car Opens in new tab. Link is a PDF document.

- Let's Talk Taxes Opens in new tab. Link is a PDF document.

- Living on Your Own Opens in new tab. Link is a PDF document.

- Loan Basics Opens in new tab. Link is a PDF document.

- Organizing Your Finances Opens in new tab. Link is a PDF document.

- Paying for School Opens in new tab. Link is a PDF document.

- Predatory Lending Opens in new tab. Link is a PDF document.

- Protecting Yourself Online Opens in new tab. Link is a PDF document.

- Rule of 72 Opens in new tab. Link is a PDF document.

- Strategies for Debt Repayment Opens in new tab. Link is a PDF document.

- Student Loans 101 Opens in new tab. Link is a PDF document.

- The 7 Co-operative Principles Opens in new tab. Link is a PDF document.

- Understanding Credit Scores Opens in new tab. Link is a PDF document.

- Understanding Inflation Opens in new tab. Link is a PDF document.

- Using Payment Cards Opens in new tab. Link is a PDF document.

- Using Your Credit Card Opens in new tab. Link is a PDF document.

- Writing a Business Plan Opens in new tab. Link is a PDF document.